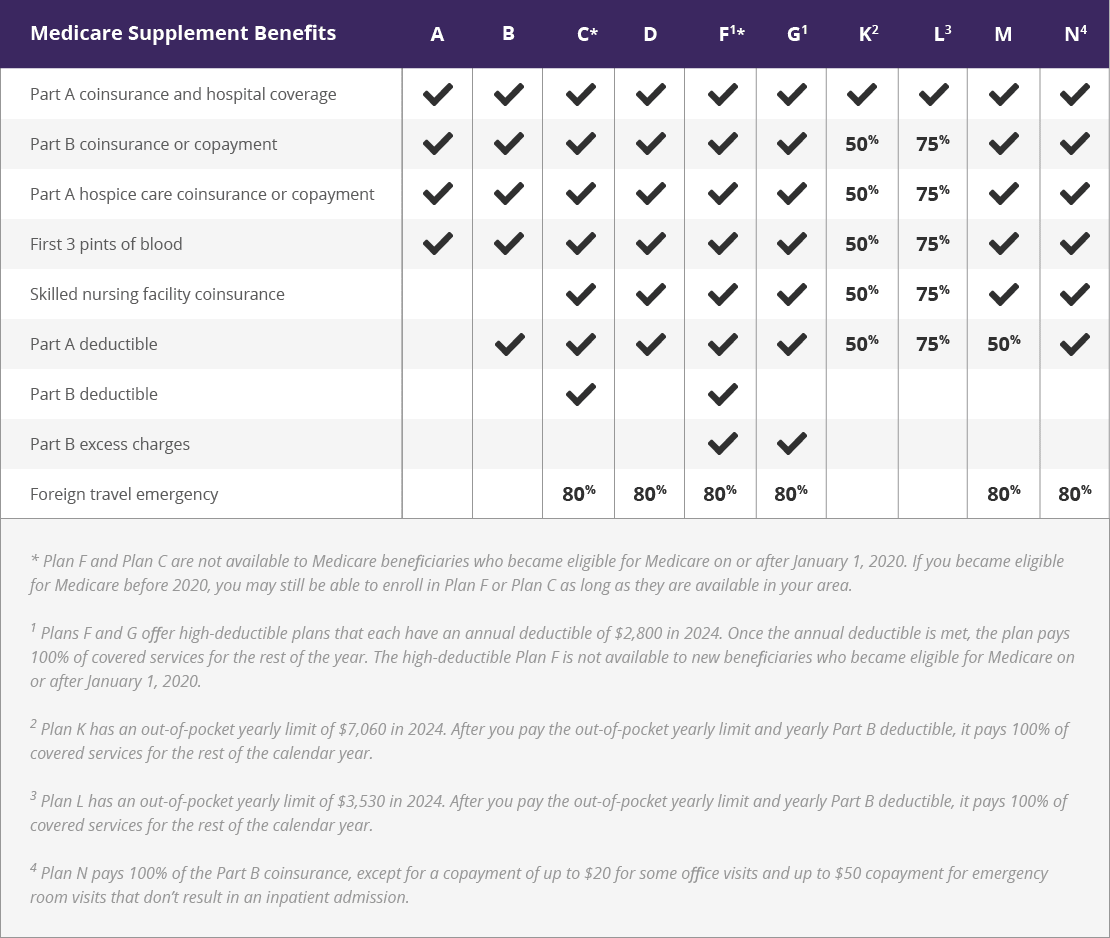

The Medicare Supplement Insurance plan comparison chart below is a great tool you can use to learn about your potential coverage options and to see which type of plan may be right for your needs.

This chart outlines the benefits that are covered by each type of Medicare Supplement Insurance plan (also called Medigap).

Medigap plan comparison chart

Click here to view enlarged chart Scroll to the right to continue reading the chart

Scroll for more

| Medicare Supplement Benefits |

A |

B |

C* |

D |

F1* |

G1 |

K2 |

L3 |

M |

N4 |

| Part A coinsurance and hospital coverage |

|

|

|

|

|

|

|

|

|

|

| Part B coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A hospice care coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| First 3 pints of blood |

|

|

|

|

|

|

50% |

75% |

|

|

| Skilled nursing facility coinsurance |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A deductible |

|

|

|

|

|

|

50% |

75% |

50% |

|

| Part B deductible |

|

|

|

|

|

|

|

|

|

|

| Part B excess charges |

|

|

|

|

|

|

|

|

|

|

| Foreign travel emergency |

|

|

80% |

80% |

80% |

80% |

|

|

80% |

80% |

What are the different Medicare Supplement plans?

As you can see from the chart above, there are 10 types of standardized Medicare Supplement Insurance plans available in most states, each identified by a letter: A, B, C, D, F, G, K, L, M and N.

Plan F and Plan G also offer a high-deductible version. High deductible Plan F and high deductible Plan G typically offer lower monthly premiums in exchange for having a high deductible that must be met before plan coverage kicks in.

What can Medicare Supplement Insurance plans cover?

Medigap plans can cover up to nine of the following out-of-pocket 2026 Medicare costs. Each type of plan will offer a different combination of some or all of these benefits:

- Part A deductible

Medicare beneficiaries must meet a $1,736 deductible for each benefit period in 2026 before Medicare Part A covers any inpatient hospital costs.

- Part A coinsurance and hospital costs

In 2026, Medicare Part A coinsurance is $434 per day for days 61-90 of an inpatient hospital stay, and $868 per day thereafter.

- Part B deductible

The Medicare Part B deductible in 2026 is $283 per year.

- Part B coinsurance and copayments

Medicare Part B requires a 20 percent coinsurance payment for all covered services and medical equipment once the annual Part B deductible is met.

- Part A hospice care coinsurance

Part A may charge minor copayments for prescription drugs related to hospice service and a 5 percent coinsurance payment for inpatient respite care.

- Skilled nursing facility coinsurance

Medicare Part A charges a copayment of $217 per day in 2026 for days 21-100 of an inpatient stay at a skilled nursing facility.

- Part B excess charges

If you receive Part B services from a health care provider that does not accept Medicare assignment, you may be subject to excess charges of up to 15 percent of the Medicare-approved amount for the service.

- First three pints of blood

Original Medicare does not cover the costs for the first three pints of blood used in a transfusion or a medically necessary procedure.

- Foreign travel emergency care

Emergency medical care that is received outside of the U.S. is not typically covered by Original Medicare, except under special circumstances.

5 important things to note about Medigap plans

There are a few things to note when analyzing the above Medicare Supplement Insurance plans comparison chart.

- The coverage provided by each type of Medicare Supplement Insurance plan is standardized, which means the benefits of each type of plan will be the same, no matter where the plan is sold.

- Not every plan type is sold in all locations. People in some states may have access to more types of Medigap plans than people in other states.

- The cost of plans can vary based on location, provider and coverage offered. Plans with more benefits typically cost more than plans with less coverage.

- High-Deductible Medigap Plan F and high-deductible Medigap Plan G are two plan options beneficiaries can consider. These two plans require the plan holder to meet a $2,950 annual deductible in 2026 before the plan covers any benefits.

- Two types of plans provide an annual out-of-pocket spending limit. Medigap Plan L ($4,000 in 2026) and Plan K ($8,000 in 2026) cover 100% of Original Medicare expenses for the rest of the calendar year once a beneficiary reaches these spending limits.

As of January 1, 2020, Plan F and Plan C are longer available to new Medicare beneficiaries. If you already were eligible for Medicare before Jan. 1, 2020, you may be able to enroll in Plan F or Plan C if either is available in your area.

Most Popular Medigap Plans

The most popular Medigap plan is Plan F, which is the only plan to provide maximum coverage in each benefit area.

Because Plan F is not available for new beneficiaries who became eligible for Medicare after January 1, 2020, Plan G will likely become the most popular Medigap plan for new Medicare beneficiaries.

Plan G covers more Medigap benefit areas than any other Medigap plan (other than Plan F).

How Do You Compare Medigap Plans?

There are a few things to keep in mind when comparing Medigap plans.

First, keep in mind that Medigap coverage is standardized, which means a plan of any given letter will offer the same coverage as another plan by the same letter, no matter where they were purchased.

So for example, Medigap Plan N in New York will offer the same standardized benefits as Plan N in California.

Next, ask yourself some questions such as:

- Which Medigap benefits are most important to you?

- How do you typically utilize your Medicare coverage? Do you see the doctor regularly?

- Do you travel or frequently visit non-participating providers?

Next, you’ll want to compare plan availability and costs in your area.

Not all Medigap plans are available in every location, so some types of plans may or may not be available where you live.

The cost of plans can vary based on different factors, including your location and the insurance company who provides the plan, so you may want to consider the costs of each type of plan that's available near you.

One way to compare Medigap plans is to get in touch with a licensed insurance agent who can help you review the selection of plans available in your area. To get help finding the right plan for your needs, you can visit MedicareSupplement.com.

Medigap Plan N vs. Plan G

Medigap Plan N and Plan G offer the same standardized benefits except for one area: Plan G provides coverage of Medicare Part B excess charges while Plan N does not.

You may face Part B excess charges if you visit a health care provider who does not accept Medicare assignment. This means they reserve the right to charge up to 15% more than the Medicare-approved amount for covered services or items.

If your favorite doctor does not accept Medicare assignment, or if you do a fair amount of traveling around the U.S. and could potentially need to seek care from a provider who doesn't accept Medicare assignment, you may want to consider Plan G to have full coverage of any Part B excess charges.

However, if you only visit providers who accept assignment (most providers do accept Medicare assignment), and Plan N is more affordable in your area than Plan G, you may be better off selecting Plan N.

This is just one example of how you might compare one plan to another to get an idea of how each plan may fit in with your health care needs.

Learn more about Medicare Supplement Insurance plans

The best time to enroll in a Medicare Supplement Insurance plan is during your Medigap Open Enrollment Period. This six-month period begins as soon as you are 65 years old and enrolled in Medicare Part A and Part B.

If you enroll in a Medigap plan outside of your Medigap Open Enrollment Period, you may be subject to medical underwriting by the insurance company selling the plan. This means that you could be charged higher premiums or denied a policy altogether based on your age and health.

To get help using the Medicare Supplement Insurance plans comparison chart and to find the right plan for your needs, visit MedicareSupplement.com today!

Learn more about Medigap plans in your area

Speak with a licensed insurance agent

{kind=link}